Blog Post

June 26, 2026

Airs live on YouTube

June 26, 2026

Inflation Rose, but Mortgage Rates Improved. Here’s What Buyers Should Know.

Education

Coming Soon

Follow us on YouTube to watch live!

A hot inflation report could have pushed mortgage rates higher.

Instead, rates improved.

Inflation rose to its highest level since 2023, but markets were already looking ahead. The report reflected May, when oil was near $100 a barrel. Oil has since fallen below $70, Treasury yields moved lower, and mortgage rates followed.

Why does that matter for homebuyers?

Because rates don’t have to wait for the Fed to act before moving in a better direction. Even a modest improvement can lower a monthly payment, increase purchasing power, or bring a home that felt just out of reach back into the conversation.

New-home sales also fell 7.3% in May, another sign that affordability continues to shape the market. Anyone comparing new construction with resale homes should look at the full picture, including financing options, builder incentives, and total monthly cost.

The perfect market may never arrive, but better opportunities can open quickly.

Know your numbers now, so you’re ready when conditions improve.

Reach out, and we’ll show you what this week’s rate movement could mean for your homebuying plan.

Featuring:

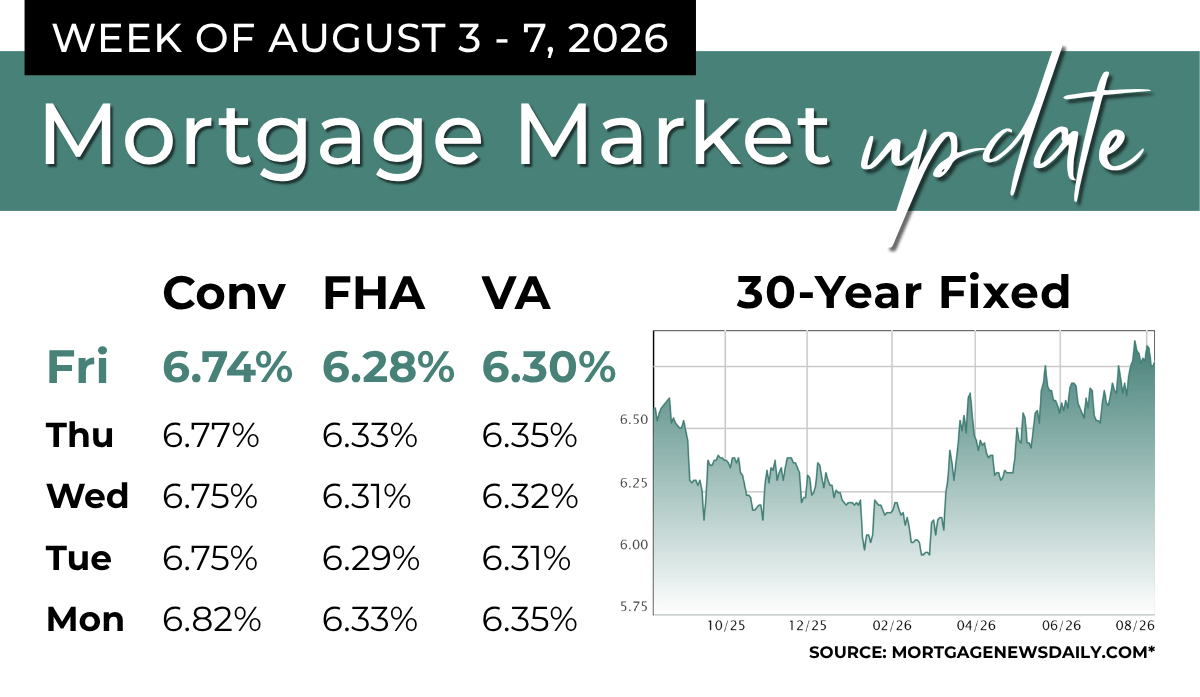

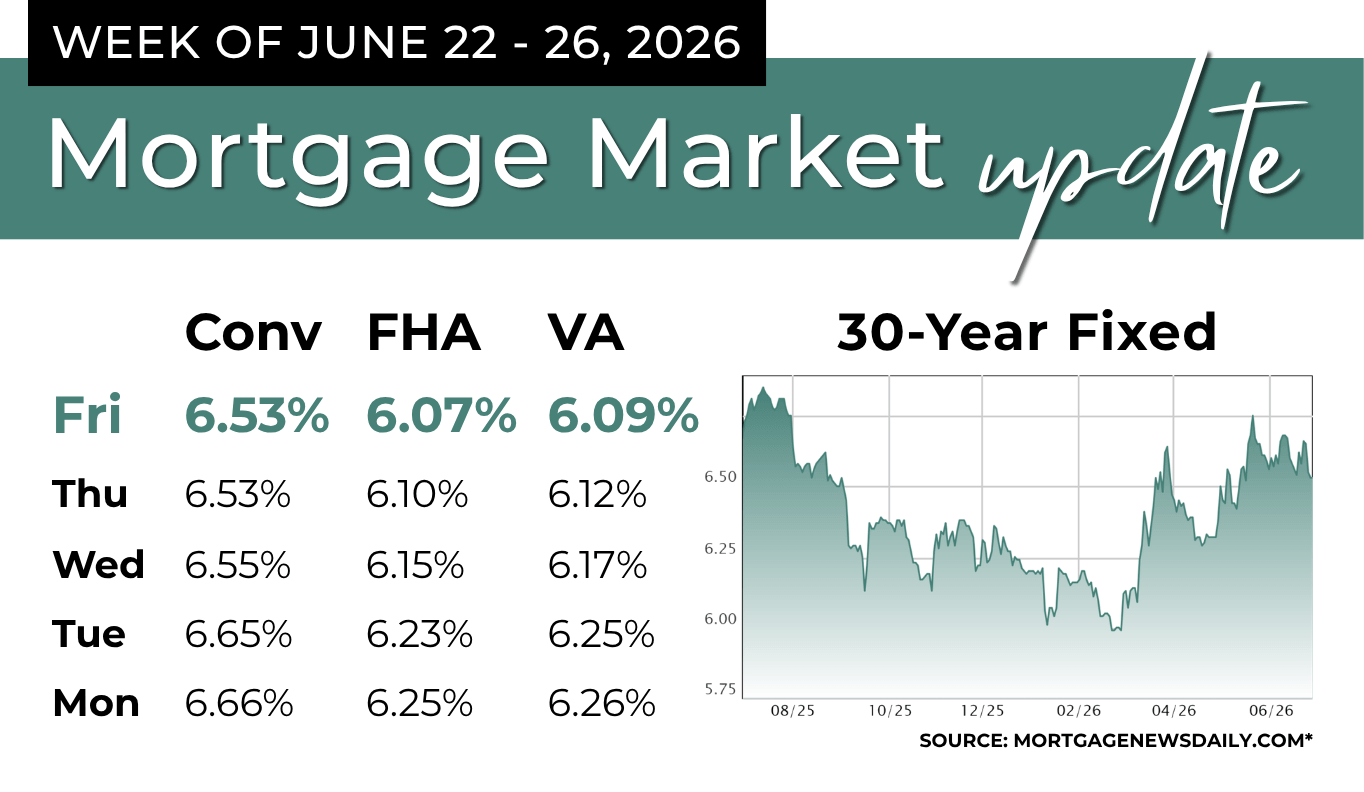

Rate Source: MortgageNewsDaily.com

*The Mortgage News Daily index attempts to capture the most prevalently quoted conventional, FHA, and VA 30-year fixed rates for highly qualified homebuyers that meet the appropriate down payment requirements and have no major loan-level price adjustments.

Mortgage News Daily is a trademark of Mortgage News Daily, LLC. CrossCountry Mortgage, LLC; its subsidiaries; and its affiliates have not been authorized, sponsored, or otherwise approved by Mortgage News Daily, LLC or any of the above-mentioned companies.