Blog Post

June 25, 2026

Airs live on YouTube

June 25, 2026

Your House Didn’t Sell. Here’s How To Turn It Around.

Education

Coming Soon

Follow us on YouTube to watch live!

You started shopping with a specific mental image of your future home in your mind. Then the houses in your budget came in smaller than you pictured.

That’s the reality for a lot of buyers right now. Affordability is tight.

But don’t let that discourage you. Going smaller might actually be a smart play in today’s market – and the upside can be bigger than you’d think. Let’s break down two places to look where smaller won’t necessarily feel like a compromise.

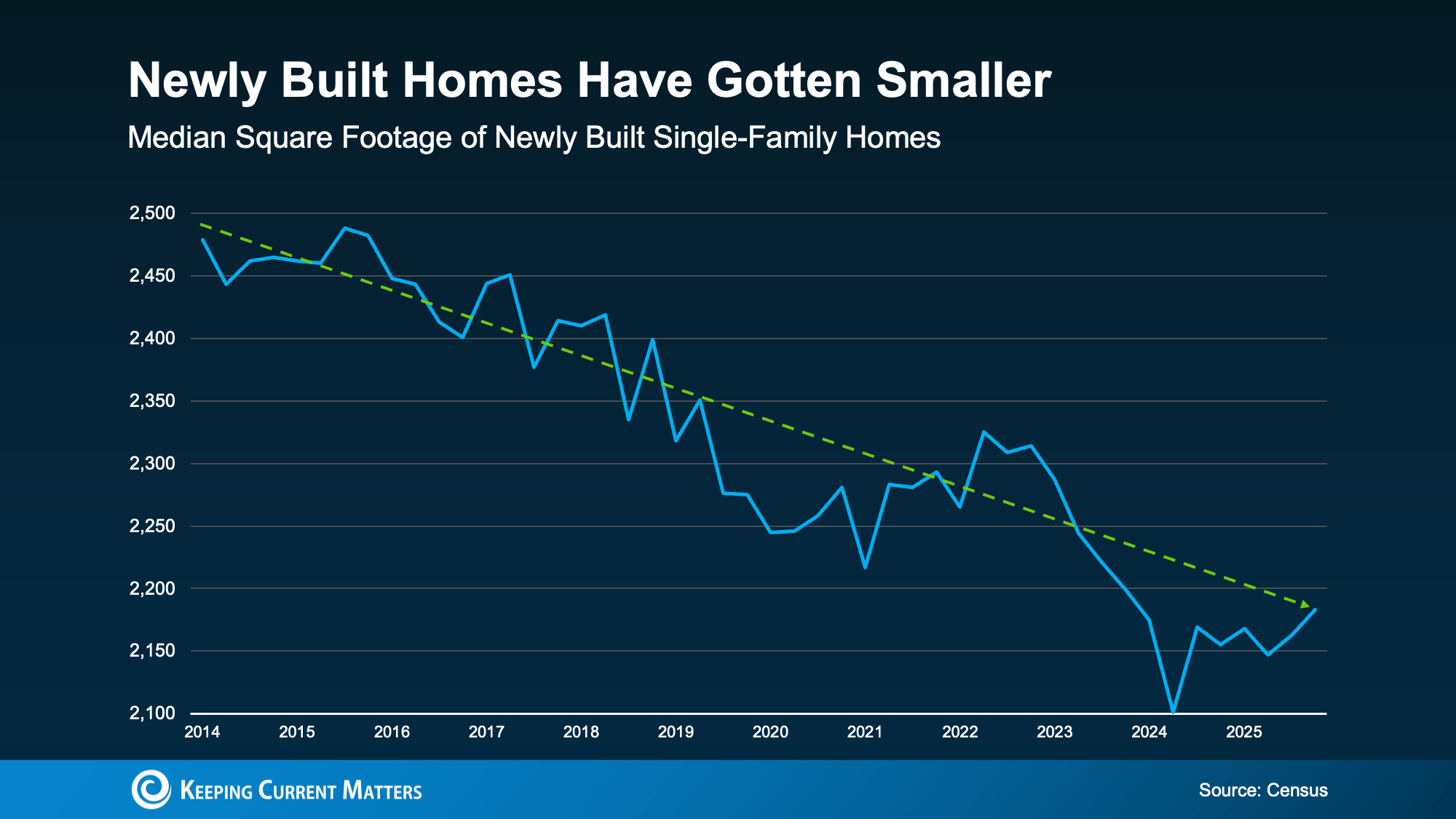

Homebuilders Are Focused on Smaller Options Lately

For starters, smaller is kind of on trend right now. Newly built homes have been shrinking for years. According to the latest data from the Census, the median square footage of new single-family homes has been falling overall since 2014 (see graph below):

Why? Builders focus on the types of homes consumers want the most. After all, they want to build what will actually sell. And for the past decade, buyers seem to agree less is more.

Especially right now, when affordability is a key concern, they’re building homes with smaller square footage than a decade ago. And that’s good because that may be more within budget for many buyers. It’s part of why new home prices recently hit a 5-year low.

So, if you’re not getting excited about any of the existing options at your price point, it may be time to check out what builders are doing in your area.

You may find brand-new options you really love with all the latest and greatest features. And if you’ve got modern appliances and design, maybe slightly less square footage doesn’t feel like that much of a compromise anymore, especially if the house is move-in ready.

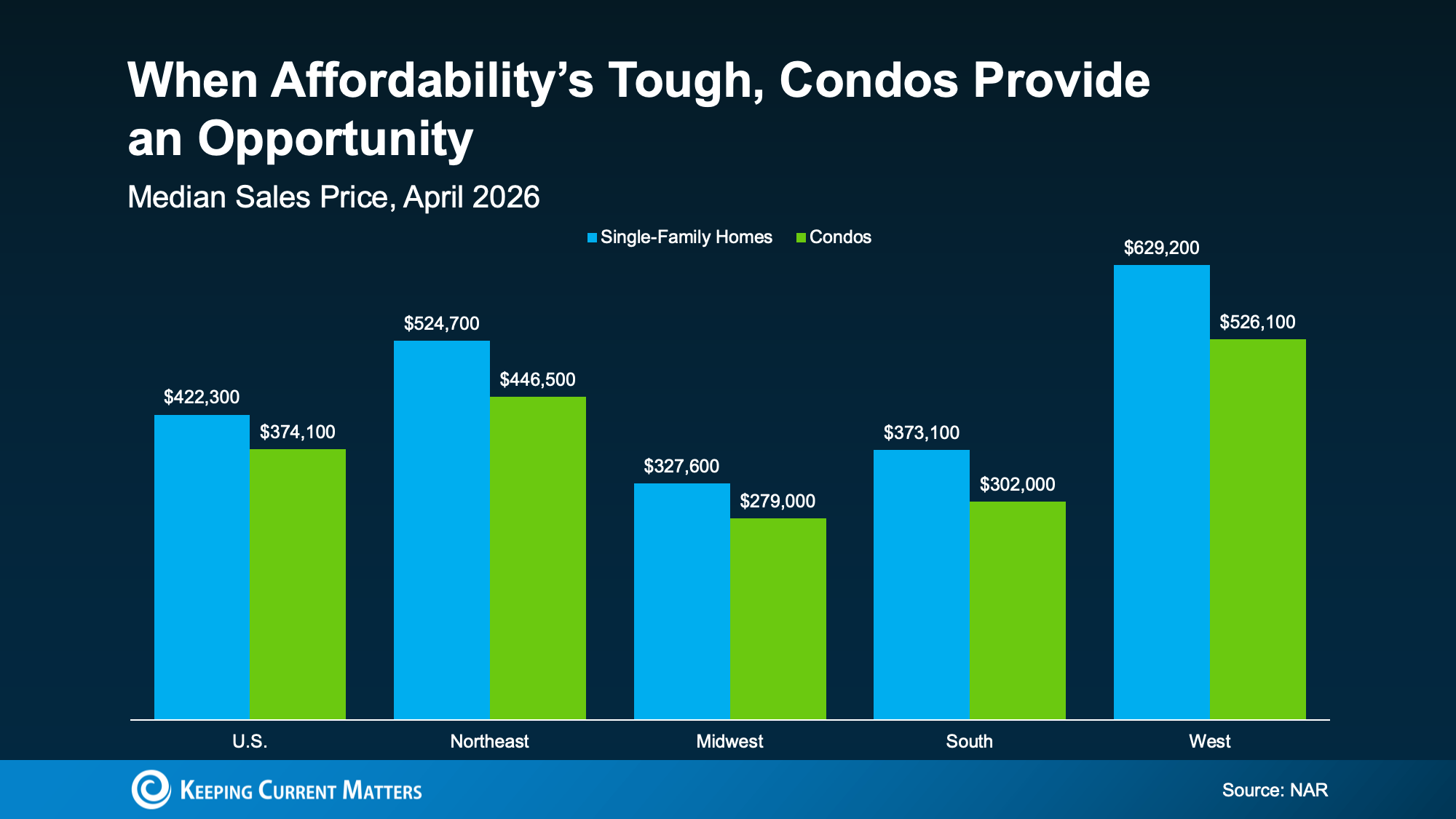

Condos Are Opening Up Another Path

Just in case you don’t have a ton of new builds in your area, another avenue worth exploring is condominiums or condos.

For buyers crunching numbers to make the math work, condos can take real pressure off the budget. According to the National Association of Realtors (NAR), the median price for condos is less than the median for single-family homes in every region (see graph below):

Part of that is because condos are typically smaller. And smaller square footage can come with a smaller price tag too. That’s a selling point to affordability-strapped buyers right now – and it’s one of the reasons we’re seeing a bump in condo sales.

The number of condos sold rose 2.7% from just a month ago. It’s also up year over year, according to NAR. Ali Wolf, Chief Economist for New Home Source, explains why more buyers are going this route:

“In addition to favoring smaller floor plans, more consumers are showing a willingness to live in an attached home. This shift is not driven by a preference for shared walls, but by a pursuit of value.”

The Community Does Some of the Heavy Lifting

Here’s why smaller may still work for you. Whether it’s a condo complex or a neighborhood of detached single-family homes, the right community can give you back in amenities what you trade in square footage.

Many developments are designed so the home is just one piece of where you actually spend your time. Master-planned communities often include walking trails, pools, fitness centers, co-working spaces, and outdoor gathering areas – the kind of features that pick up where your floor plan leaves off.

No room for a dedicated office? The co-working space might be just a five-minute walk away. Want a place to work out? It’s already built in with the shared gym. And features like that can make opting for a smaller footprint feel less like a compromise – and more like a big lifestyle upgrade.

Bottom Line

Today’s smaller single-family homes and condos have more going for them than the square footage suggests. They can give your budget some breathing room and put you in a community designed with lifestyle in mind.

Curious about the options in your area? Let's chat to walk through what's available.

Featuring:

Source: Keeping Current Matters

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Keeping Current Matters is a trademark of Keeping Current Matters, Inc. CrossCountry Mortgage, LLC; its subsidiaries; and its affiliates have not been authorized, sponsored, or otherwise approved by Keeping Current Matters, Inc. or any of the above-mentioned companies.