Blog Post

June 18, 2026

Airs live on YouTube

June 18, 2026

Is It Still a Seller's Market? Here's What the Data Says.

Education

Coming Soon

Follow us on YouTube to watch live!

Remember a few years back when sellers held all the power and buyers were stuck offering way over asking or waiving inspections just to get a chance at the house? In many markets, those days are behind us.

While it’s going to vary by area, more metros are slowly shifting to favor buyers, and the market is starting to look a lot more like a two-way street again.

And that balance is something we haven’t had in a while.

Whether you’re buying or selling, here’s what you need to know about what’s changing and what it means for your move.

The Most Buyer-Friendly Market in Years

The national data tells an interesting story right now. According to Realtor.com:

“The national housing market is balanced but gradually loosening as the cycle moves in a more buyer-friendly direction . . .“

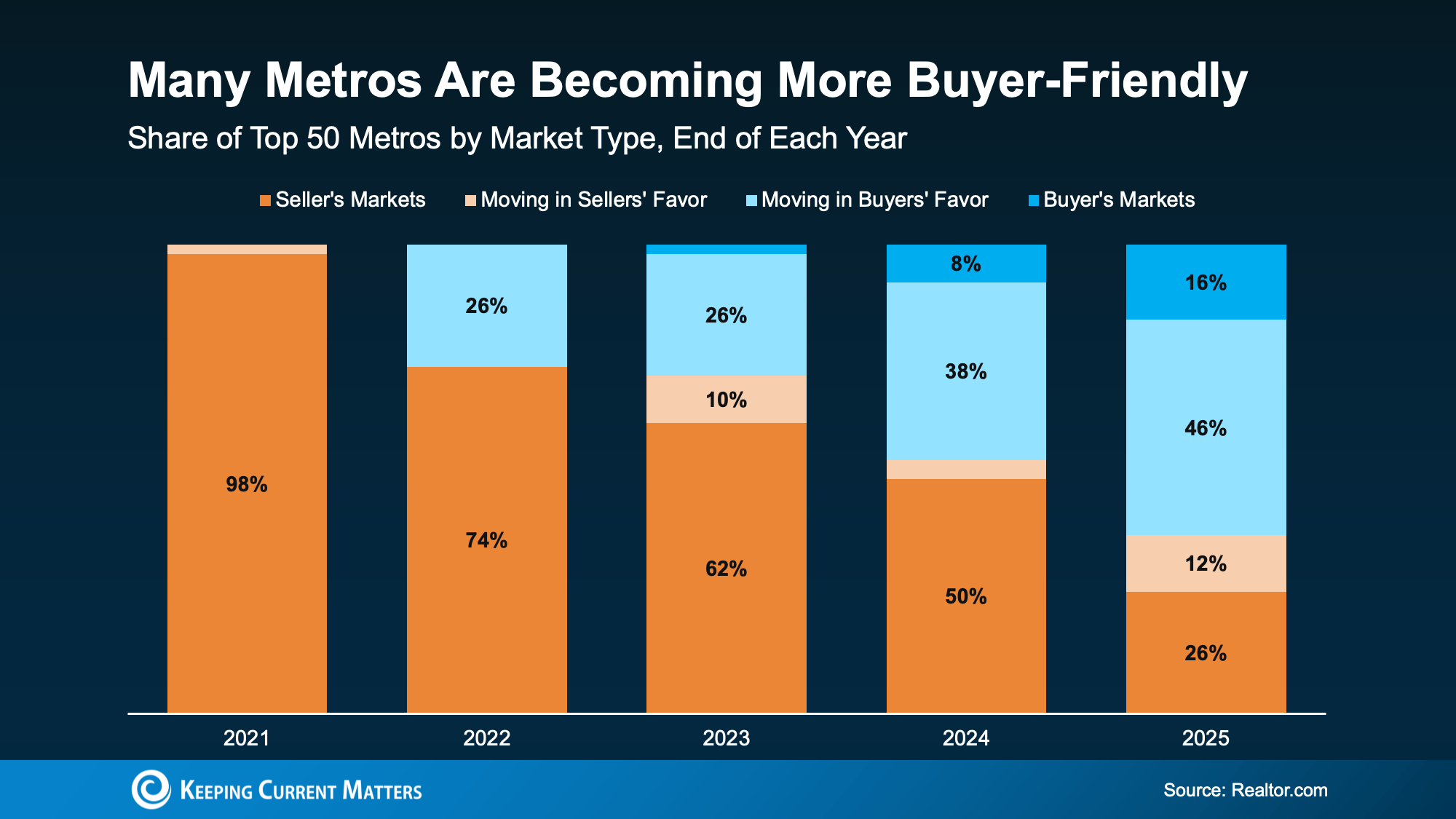

That’s because, over the past few years, more and more metros have been flipping back to more buyer-friendly terms as inventory’s grown. And when you zoom in on the latest Realtor.com data for the top 50 metro markets over time, the trend becomes really clear (see graph below).

Back in 2021, almost all major metros were seller’s markets. By the end of 2025, only 1 in 3 still favored sellers. That’s an obvious shift.

And that changes how the market is going to feel for everyone. Sellers shouldn’t still expect 2021 conditions, but neither should buyers. At least, not generally speaking.

It’s Not the Same Story Everywhere

That said, who has the power ultimately depends on where you live. While more metros are leaning buyer-friendly lately, there are still plenty of strong seller’s markets right now, too.

It really comes down to how much housing supply and demand there is in your area. And that varies enormously by region.

Sun Belt cities like Austin, Tampa, and San Antonio saw major building booms in recent years, giving buyers more options and more negotiating room. Meanwhile, cities in the Northeast and Midwest – think Rochester, Hartford, and Buffalo – didn’t see that same wave, so inventory stayed tight and competition stayed fierce. As Jeff Ostrowski, Housing Analyst at Bankrate, explains:

“The formerly hot Sun Belt markets have cooled, while the Northeast and Midwest have stayed hot. The big driver here is construction activity. The softest markets now [have] experienced big booms that spurred new building, and that has led to a large supply of new and existing homes on the market in those places.”

Practical Advice for Your Move

To find out who has the power in your local market, talk to an agent. Because knowing what’s happening locally is going to be the key to setting the right strategy for your move.

If the market is working in your favor, great. Lean in and use it to your benefit. But if it’s not, all hope isn’t lost. Your agent can help you figure out how to approach any market.

Here’s some practical advice if there’s a mismatch between your goal and local market conditions.

If you’re buying in a seller’s market:

-

Get pre-approved before you start shopping. It shows sellers you’re serious.

-

Be ready to act fast when the right home hits the market.

-

Consider offering a quick closing date or flexible terms.

-

Work closely with your agent to craft a competitive offer.

If you’re selling in a buyer’s market:

-

Price it right from day one. Overpricing will cost you time and money.

-

Focus on curb appeal and staging to stand out in areas with more inventory.

-

Be open to offering incentives, like covering closing costs or a home warranty.

-

Expect buyers to negotiate and be ready to be flexible.

Bottom Line

Right now, local markets are moving in very different directions. And your strategy as a buyer or seller should reflect your market.

Want to know which way your local market is leaning and what that means for your move? Let's connect.

Featuring:

Source: Keeping Current Matters

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Keeping Current Matters is a trademark of Keeping Current Matters, Inc. CrossCountry Mortgage, LLC; its subsidiaries; and its affiliates have not been authorized, sponsored, or otherwise approved by Keeping Current Matters, Inc. or any of the above-mentioned companies.